French Finance Bill 2026: Key Tax Measures for Businesses

On Tuesday, October 14, the new government led by Sebastien Lecornu presented the Finance Bill for 2026, in compliance with the 70-day period granted to Parliament to deliberate.

The Finance Bill 2026 (PLF 2026) provides for an increase of €19.2 billion in net tax revenues compared with the revised forecast for 2025.

Out of a total of €372.9 billion in projected revenue:

• €109.1 billion will come from Value-Added Tax (VAT),

• €104 billion from income tax,

• €59 billion from corporate income tax,

• €22.9 billion from energy excise duties,

• and €77.9 billion from other net tax revenues.

Main tax measures proposed

1. Extension in 2026 of the exceptional levy on large corporate profits, with halved rates

This measure applies to around 450 companies with annual turnover of at least €1 billion in France.

• For companies with turnover between €1 billion and €3 billion, the rate will fall from 20.6 % to 10.3 %.

• For those with turnover above €3 billion, the rate will drop from 41.2 % to 20.6 %.

A modification of the smoothing mechanism for the rate is also provided for.

2. Introduction of a 2 % tax on the financial assets of holding companies

This tax would target assets with a market value of €5 billion or more, financed by accumulated profits within companies rather than distributed earnings.

It would also apply to French residents holding foreign holding structures.

3. Accelerated phase-out of the CVAE (Contribution on the Value Added of Enterprises) by 2028

Initially planned for 2024 and postponed several times until 2030, the complete abolition would now take place in 2028:

• maximum rate reduced from 0.28 % to 0.19 % in 2026,

• then to 0.09 % in 2027.

Adjustments will also be made to the ceiling rate of the CET (local business tax) and the additional CVAE levy.

4. Introduction of a €2 national fee on small parcels (value < €150) imported from non-EU countries

Pending the implementation of the EU customs reform, this measure aims to support French businesses against unfair competition from non-European e-commerce operators.

5. Adjustment of the VAT exemption threshold (franchise en base)

The reform suspended in 2025 would be revived with a single VAT registration threshold of €37,500 in annual turnover, and a specific threshold of €25,000 maintained for construction works.

Between March 1 and December 31, 2025, businesses continue to apply the thresholds in effect as of January 1, 2025.

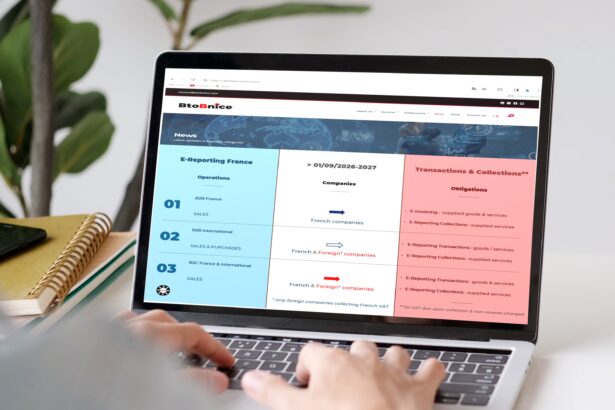

6. Revision of e-invoicing and e-reporting obligations

In addition to various simplification and clarification measures, the PLF 2026 introduces new penalties:

• failure to issue e-invoices: fine increased from €15 to €50 per invoice,

• failure to designate an approved platform: €500 fine, then €1,000 per quarter,

• non-compliance with e-reporting obligations: €500 per transmission (capped at €15,000 per year),

• for approved platforms (former PDPs): €750 per transmission (capped at €100,000 per year).

7. Elimination of various low-impact tax reliefs

A number of tax incentives are abolished, including:

• tax credits for business-owner training and employee buyouts;

• several income and corporate tax exemptions (grants, prizes, subsidies, etc.);

• the special rate for B100 biofuel;

• and the gradual reduction of the E85 biofuel tax advantage.

8. Greening of taxation

• adjustment of vehicle and transport-related taxation;

• application of a uniform 5.5 % VAT rate to waste collection and treatment services;

• introduction of a tax on plastic packaging, and other environmental measures.

9. Regulation of property tax adjustments

Adjustment of the ongoing revision of rental values for both professional and residential premises, to better control year-on-year increases.

10. Rationalization of energy taxation

Compensation for tax frictions through (VAT) a reduction in electricity excise duty.

Other sector-specific and regional provisions are also included in the Finance Bill 2026.

These may be amended or supplemented before the final adoption by the National Assembly and the Senate.

A follow-up will be provided once the Finance Law 2026 is promulgated.