VAT refund : foreign business expenses

As part of their business operations, international companies frequently incur VAT-taxed expenses abroad. These foreign expenses may include the purchase of goods and services from foreign suppliers, as well as employee business travel abroad, covering costs like hotels, restaurants, car rentals, fuel, tolls, transport, congresses, exhibitions, and more.

While foreign VAT is systematically applied to travel-related expenses, it may also be charged on supplier invoices depending on the nature and location of the purchased goods or services, and in accordance with each country’s specific VAT regulations.

Implemented in more than 175 countries, input VAT on business expenses is typically deductible for locally registered companies against the output VAT they collect on taxable sales. In addition, many jurisdictions provide foreign VAT refund schemes that allow foreign companies without local VAT registration to reclaim eligible VAT. Today, over 50 countries around the world offer VAT refunds to non-resident businesses.

Understanding Foreign VAT Refund Rules

The foreign VAT refund process varies from country to country and includes multiple criteria and requirements, such as:

- Eligibility of foreign businesses

- Refundable expense categories

- Invoices compliance

- Submission methods (direct or via a local tax representative)

- Application format (online or postal)

- VAT refund periods and claimable amounts

- Supporting document requirements (originals, copies, or scans)

- Competent tax authorities and review processes

- Filing deadlines

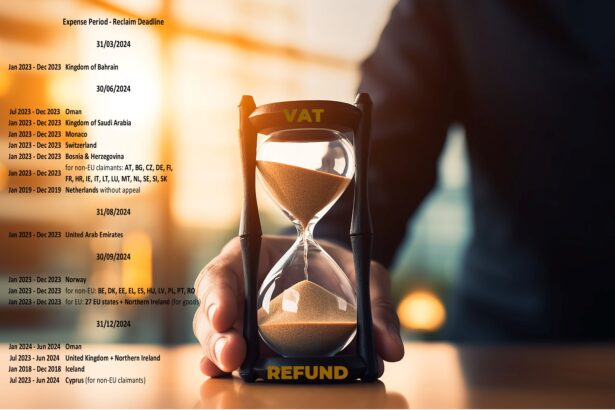

While VAT refund deadlines differ across countries, June 30 is a widely adopted annual deadline.

Deadline Alert: Claim 2024 Foreign VAT by June 30, 2025

Foreign businesses must submit their VAT refund applications for 2024 expenses no later than June 30, 2025, in the following countries:

Switzerland, Liechtenstein, Monaco, Bosnia, Montenegro, North Macedonia, Serbia, Oman, Saudi Arabia, Lebanon, Australia, South Korea, and Taiwan.

In most EU Member States, non-EU companies must also file by June 30, while EU-based businesses benefit from an extended deadline until September 30.

Other countries—including Japan, Canada, New Zealand, Bahrain, the United Arab Emirates, Oman, Turkey, the United Kingdom, Iceland, and Cyprus—have specific deadlines to consider.

To avoid rejection, it’s crucial to stay informed about local rules and file complete foreign VAT refund applications on time. Late or incomplete applications are systematically rejected by tax authorities, with no possibility of extension.

Secure Your VAT Refund with BTOBNICE

At BTOBNICE, we support international businesses in recovering their foreign VAT globally. Thanks to our VAT refund expertise and an extensive network of local partners, we ensure full compliance with refund rules and deadlines.

We manage the entire VAT refund process, from invoices selection to application filing, all the way through to obtaining official decisions and refunds. This end-to-end service enables companies to optimise and accelerate their VAT recovery, saving valuable internal resources and avoiding the complexity of country-specific regulations.

Our VAT specialists also assess the nature of your expenses to detect any taxable operations risks and adjust the refund process accordingly, securing your cross-border operations.

Contact us for expert assistance and operational support: contact@btobnice.com